By: Kristen Drake

Insurance Archeology is the practice of locating and retrieving proof of the existence, terms, conditions and limits of lost or destroyed insurance policies. Insurance Archeology is performed to find funds to pay for environmental cleanup and defend against third-party liabilities. When leveraged, these historical insurance policies are assets that can be worth millions of dollars in legal defense, cost-sharing of defense, and settlements.

A lot of people wonder how it’s possible new claims can still be made against old policies. First, you should know that these policies never expire. To explain a bit further, we are interested in Commercial General Liability or “CGL” policies. More specifically, we search for ‘occurrence-based’ policies—meaning policies which cover losses if the damage happened during the time the policy was in effect, regardless of when a claim is filed.

Regarding environmental cleanups, it’s important to note that while CGL insurance policies written prior to 1985 or 1986 contain pollution exclusions, those exclusions contain a clause that created an exception for “sudden and accidental” releases of contaminants. That exception is considered ambiguous by many courts, or they read the word sudden broadly, to, therefore, provide coverage. Old policies or evidence of insurance coverage can provide a defense against a claim or suit. In some states, a claim or suit could be a letter from the environmental regulatory agency, or a neighboring property owner – demanding a response to identified environmental contamination. In other states, the courts have determined that the insurers must only defend an actual lawsuit.

Regarding latent injury liability, like mesothelioma claims linked to asbestos exposure, old policies can be used to resolve complex claims involving events that occurred decades ago. These liabilities may be covered under old insurance policies which tend to be less restrictive and provide broader coverage. Even policies of bankrupt and defunct companies are commonly used to defend current claims. An interesting facet of Insurance Archeology is that it can be employed by either party involved in these types of lawsuits. PolicyFind is engaged equally by Plaintiffs’ Attorneys and Defense Counsel related to latent injury claims.

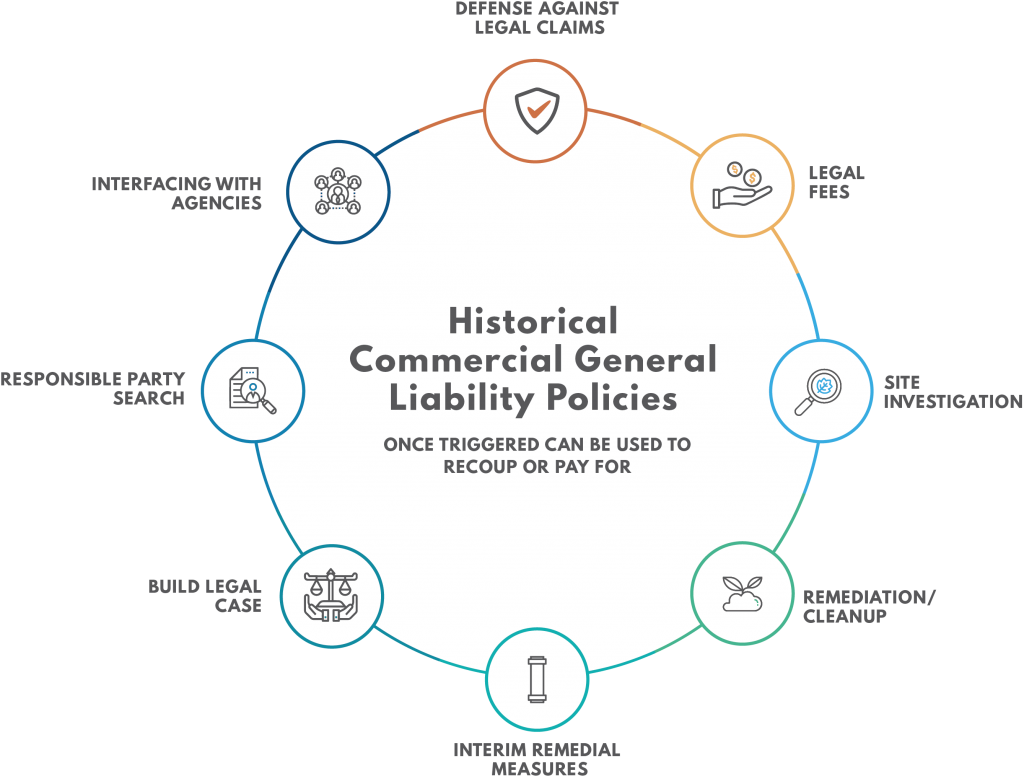

Once triggered, historical CGL policies may be used to for legal fees, defense against claims, site investigation, remediation/cleanup, interim remedial measures, building a legal case, potentially responsible party (PRP) searches, and interfacing with agencies; and, prior costs be may be retroactively recovered.

At PolicyFind, we have a disciplined process to ensure objectives are established and deliverables are beneficial and cost-effective. If you’re considering insurance archeology, here are three tips to get started.

TIP #1 – BECOME YOUR BUSINESS’ (PROPERTY’S) HISTORIAN

Try to learn what you can about former owners and/or operations before speaking with an Insurance Archeologist. If old documents no longer exist, consider making a call to former stakeholders or associates. These people might recall key pieces of information that could lead you closer to finding your old insurance coverage information. If your research efforts don’t yield the results needed to prove your historical coverage, the good news is you are now able to share what new background information you have uncovered, with an Insurance Archeologist. The more information you learn and can share, the more time the investigator can spend focusing on finding your old policies, instead of researching your business’ (property’s) history.

As it pertains to ‘old’ documents in your possession, we find many people only keep records for seven years, as this is the customary time that the IRS tells us we need to keep records for audit purposes. If ‘old records’ exist, as a ‘Historian’, it is your job to assume there is no such thing as a useless piece of paper. Certain documents may seem unimportant or irrelevant to an insurance investigation, but those are exactly the records that could provide valuable clues to the trained expert. Items of importance could include receipts, old financial ledgers, deeds, and leases. Gather what you are able and be prepared to share what you’ve learned with your Insurance Archeologist.

TIP #2 – COLLECT TOGETHER ALL YOUR INSURANCE POLICIES AND EVIDENCE OF INSURANCE

Business and property owners should make it a high priority to search, locate and securely store all of their old insurance policies and any evidence that may support that they had historical insurance. Looking for insurance coverage reduces personal liability and maintains the value of businesses.

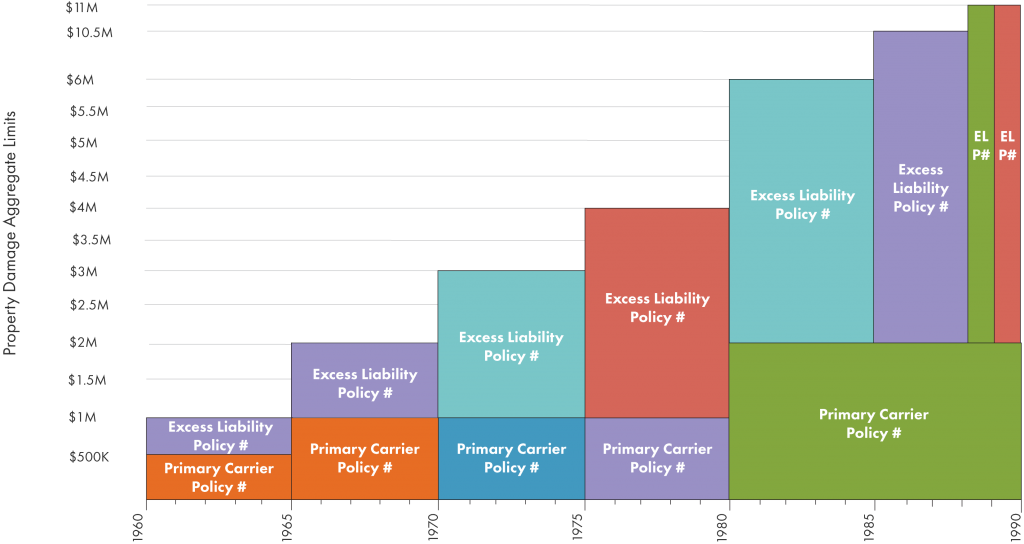

Pull together your Commercial General Liability or CGL policies, which are your normal everyday business insurance policies. Other policies can also be valuable – those include the Excess or Umbrella Liability policies, property insurance policies and Directors & Officers Liability policies, which are policies that insure business owners against claims for property damage and bodily injury.

TIP #3 – CALL AN INSURANCE ARCHEOLOGIST AND DISCUSS YOUR OPTIONS

Because there is no “one-size fits all” approach to Insurance Archeology, each investigation to locate historical insurance assets is as different and varied as our clients and their set of circumstances. The best way to accurately assess whether insurance archeology is the right option for you is to speak with an insurance archeologist who can learn more about your situation and advise you accordingly.

Insurance Archeologists do much more than just dig through files. Because no vault or database exists in which old insurance information is held, we conduct personal interviews, review public records, and we review any and all business records to look for new leads.

PolicyFind shares a common goal with our clients – to find historical insurance assets that can respond to long-tail liability and/or latent injury claims. Our collaboration with our clients begins with an initial discussion. To that end, PolicyFind’s experienced insurance archeologists offer our future clients a free initial consultation to determine potential paths forward to cost recovery.

For a confidential consultation, please fill out our form.

Kristen Drake, Director of Operations

Kristen combines her profession as an insurance archeologist with over 10 years as an investigative journalist to reconstruct historical insurance coverage for clients. She has successfully located evidence of liability insurance coverage on over 250 projects. Kristen works on behalf of policyholders defending against environmental toxic tort and asbestos exposure, carriers seeking cost allocation, and plaintiffs and defense attorneys representing clients within asbestos claims.